The Seattle rental market is in a period of real but manageable softness: renter demand has pulled back, apartment landlords are aggressively competing for tenants, and the local economy is showing strain. But for single-family rental owners who understand what's driving these shifts — and position their properties accordingly — the fundamentals still support long-term ownership, and a recovery appears to be building on the horizon.

Here's what the data says, and what it means for how you manage your investment today.

1. Renter demand is moderating across the region.

Seattle has been one of the country's strongest rental markets for the better part of two decades, powered by tech-sector growth, a steady influx of international talent, and a cultural pull that drew young professionals from across the country. That combination is still largely intact, but it's working less forcefully than it did even three years ago.

Population growth in the Seattle metro has slowed from an average of 1.6% annually during the 2010s to roughly 1.0% in 2025. On the surface, 1% annual growth still sounds healthy — and relative to many U.S. metros, it is. But the composition of that growth has changed in ways that matter for rental demand. International immigration, which historically drove a disproportionate share of renter household formation in Seattle, has declined significantly. At the same time, domestic outmigration — residents leaving for lower-cost metros in the South and Mountain West — has continued, partially offsetting incoming population.

The practical result for rental property owners is a shallower pool of prospective tenants. Properties that would have received multiple applications within days of listing are now sitting on the market longer, and pricing that felt conservative two years ago may need to be revisited.

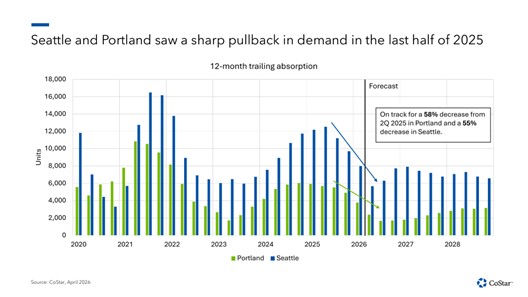

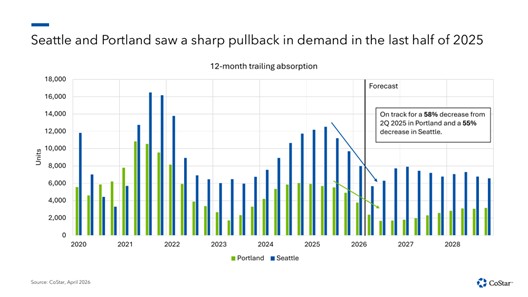

Apartment absorption in Seattle is on track for a 55% decline from Q2 2025 levels, reflecting a sharp pullback in renter demand. Source: CoStar, April 2026.

2. The local economy is showing some softness.

Employment is the single most important driver of rental demand in any market, and Seattle's job picture is more mixed than the city's tech-forward reputation might suggest. As of early 2026, Seattle employment is essentially flat year-over-year — barely negative, but a stark contrast to the consistent 2–3% annual job growth the region posted through most of the prior decade.

Some of this reflects broader national trends: the national employment growth rate has also softened to just 0.2%. But Seattle is underperforming even that modest benchmark. The slowdown is concentrated in trade-dependent sectors affected by shifting port volumes and in parts of the tech sector navigating AI-driven reorganization — a dynamic that cuts both ways, since AI investment is also creating new hiring in the region.

What this means for landlords is straightforward: tenants are more financially cautious than they were two or three years ago. Inflation has recently outpaced wage growth in Seattle, which squeezes household budgets and makes renters more sensitive to price. Rent increases that a tenant might have accepted without negotiation in 2022 are now legitimate lease-renewal friction points.

This doesn't mean rents need to fall — but it does mean that retention has become more valuable, and the cost of turnover (vacancy, make-ready expenses, leasing fees) is higher in a softer market.

3. Apartment competition has increased.

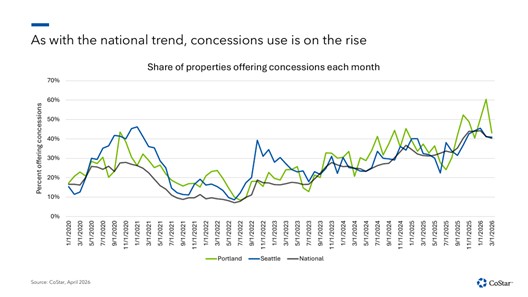

One of the most consequential dynamics for single-family rental owners right now isn't happening in the SFR market directly — it's happening in the apartment market. Following a construction boom that delivered a large volume of new multifamily units across the Seattle metro, apartment landlords are sitting on elevated vacancy and responding with concessions.

Nearly 40–45% of apartment properties in Seattle are currently offering some form of concession — free rent, reduced deposits, waived fees. When those concessions are factored into the effective rent, the true cost of many new apartments is meaningfully lower than the asking price suggests.

The share of Seattle apartment properties offering concessions has climbed back toward multi-year highs, creating direct pricing competition for single-family rentals. Source: CoStar, April 2026.

This matters for single-family rental owners because the renter who might otherwise choose your three-bedroom home is now being courted by a newly built apartment offering six weeks of free rent. The single-family rental product has inherent advantages — space, privacy, a yard, no shared walls — but those advantages need to be priced and communicated clearly to win in the current environment.

Practically, this means property managers should be conducting regular rent comp analyses that account for effective apartment rents, not just asking rents. A single-family home priced as if it's competing against face-rent apartments may be inadvertently overpriced relative to what renters can actually find in the market.

4. Well-maintained homes continue to outperform.

Not all rental properties are experiencing the same pressure. Across the Seattle market, a clear pattern has emerged: higher-quality, well-maintained properties are holding occupancy and achieving better rents, while older properties with deferred maintenance are losing ground at a faster rate.

This flight-to-quality dynamic is partly a function of the concession environment. When renters have more options and more negotiating leverage, they gravitate toward the best available product at a given price point. A dated kitchen or aging flooring that went unnoticed in a tight 2021 market becomes a reason to pass in 2026.

For single-family rental owners, this is both a warning and an opportunity. Properties that have been maintained and selectively updated — particularly in kitchens, bathrooms, and curb appeal — are differentiating themselves from the competition in a way that supports both occupancy and rent. Properties where maintenance has been deferred are facing longer vacancies and pressure to reduce asking rent.

If you've been weighing whether to invest in improvements, the current market argues for moving sooner rather than later.

5. The near-term outlook points toward stabilization.

The softness in the Seattle rental market is real, but it's not a structural collapse — and the conditions for recovery are already taking shape. New apartment construction has dropped sharply, with deliveries falling more than 50% over the past year. Historically, that kind of supply pullback — combined with a population base that is still growing, if more slowly — sets the stage for tighter vacancy and recovering rents.

Forecasters currently point toward a meaningful improvement beginning in 2027. That's not far away, and for long-term rental owners, the current period looks more like a cycle trough than a new normal. Owners who use this time to improve their properties, price strategically, and retain good tenants are likely to be well-positioned when conditions shift.

The Seattle market's underlying drivers — its educated workforce, its role in the technology economy, its geography — remain intact. The investors who treat this moment as a reason to manage more carefully, rather than panic, will be the ones who look back on 2026 as an opportunity.

Data sourced from CoStar Q2 2026 State of the Market: Seattle/Portland. Market conditions are subject to change. This post is intended for informational purposes and does not constitute investment advice. Contact your property management team for guidance specific to your portfolio.

Updated 6/1/2026 10:26AM PDT.